fuck it

its not *my* debt

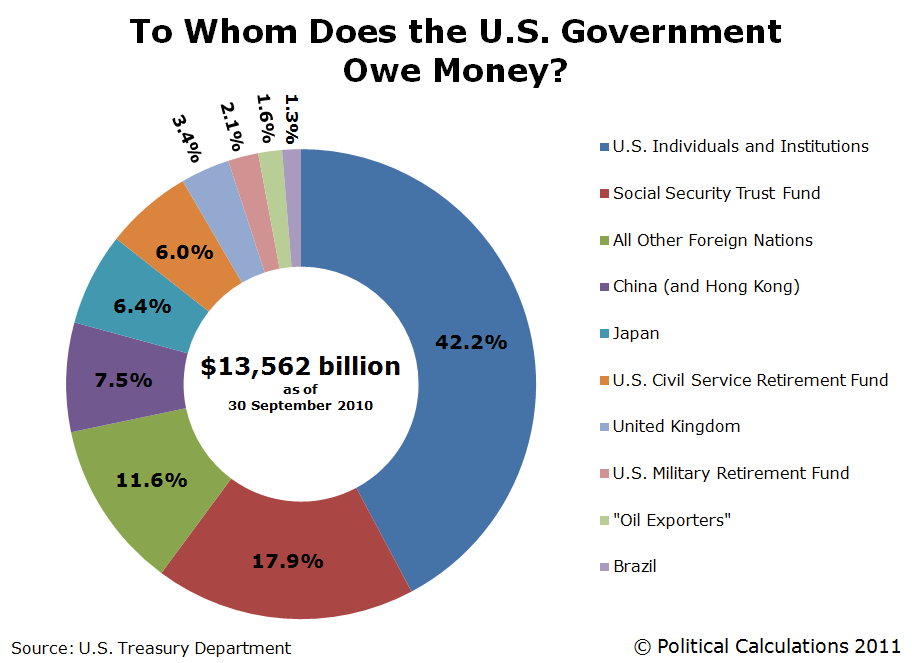

(heavily edited)

In the spring of 1981, conservative Republicans in the House of Representatives cried. They cried because, in the first flush of the Reagan Revolution that was supposed to bring drastic cuts in taxes and government spending, as well as a balanced budget, they were being asked by the White House and their own leadership to vote for an increase in the statutory limit on the federal public debt, which was then scraping the legal ceiling of $1 trillion. They cried because all of their lives they had voted against an increase in public debt, and now they were being asked, by their own party and their own movement, to violate their lifelong principles. The White House and its leadership assured them that this breach in principle would be their last: that it was necessary for one last increase in the debt limit to give President Reagan a chance to bring about a balanced budget and to begin to reduce the debt. Many of these Republicans tearfully announced that they were taking this fateful step because they deeply trusted their president, who would not let them down.......................

Before the Reagan era, conservatives were clear about how they felt about deficits and the public debt: a balanced budget was good, and deficits and the public debt were bad, piled up by free-spending Keynesians and socialists, who absurdly proclaimed that there was nothing wrong or onerous about the public debt. In the famous words of the left-Keynesian apostle of "functional finance," Professor Abba Lernr, there is nothing wrong with the public debt because "we owe it to ourselves." In those days, at least, conservatives were astute enough to realize that it made an enormous amount of difference whether — slicing through the obfuscatory collective nouns — one is a member of the "we" (the burdened taxpayer) or of the "ourselves" (those living off the proceeds of taxation).......................................

To think sensibly about the public debt, we first have to go back to first principles and consider debt in general. Put simply, a credit transaction occurs when C, the creditor, transfers a sum of money (say $1,000) to D, the debtor, in exchange for a promise that D will repay C in a year's time the principal plus interest. If the agreed interest rate on the transaction is 10 percent, then the debtor obligates himself to pay in a year's time $1,100 to the creditor. This repayment completes the transaction, which in contrast to a regular sale, takes place over time.

So far, it is clear that there is nothing "wrong" with private debt. As with any private trade or exchange on the market, both parties to the exchange benefit, and no one loses. But suppose that the debtor is foolish, gets himself in over his head, and then finds that he can't repay the sum he had agreed on? This, of course is a risk incurred by debt, and the debtor had better keep his debts down to what he can surely repay. But this is not a problem of debt alone. Any consumer may spend foolishly; a man may blow his entire paycheck on an expensive trinket and then find that he can't feed his family. So consumer foolishness is hardly a problem confined to debt alone. But there is one crucial difference: if a man gets in over his head and he can't pay, the creditor suffers too, because the debtor has failed to return the creditor's property. In a profound sense, the debtor who fails to repay the $1,100 owed to the creditor has stolen property that belongs to the creditor; we have here not simply a civil debt, but a tort, an aggression against another's property.........................

Most people, unfortunately, apply the same analysis to public debt as they do to private. If sanctity of contracts should rule in the world of private debt, shouldn't they be equally as sacrosanct in public debt? Shouldn't public debt be governed by the same principles as private? The answer is no, even though such an answer may shock the sensibilities of most people. The reason is that the two forms of debt-transaction are totally different. If I borrow money from a mortgage bank, I have made a contract to transfer my money to a creditor at a future date; in a deep sense, he is the true owner of the money at that point, and if I don't pay I am robbing him of his just property. But when government borrows money, it does not pledge its own money; its own resources are not liable. Government commits not its own life, fortune, and sacred honor to repay the debt, but ours. This is a horse, and a transaction, of a very different color.................................

The public debt transaction, then, is very different from private debt. Instead of a low-time-preference creditor exchanging money for an IOU from a high-time-preference debtor, the government now receives money from creditors, both parties realizing that the money will be paid back not out of the pockets or the hides of the politicians and bureaucrats, but out of the looted wallets and purses of the hapless taxpayers, the subjects of the state. The government gets the money by tax-coercion; and the public creditors, far from being innocents, know full well that their proceeds will come out of that selfsame coercion. In short, public creditors are willing to hand over money to the government now in order to receive a share of tax loot in the future. This is the opposite of a free market, or a genuinely voluntary transaction. Both parties are immorally contracting to participate in the violation of the property rights of citizens in the future. Both parties, therefore, are making agreements about other people's property, and both deserve the back of our hand. The public credit transaction is not a genuine contract that need be considered sacrosanct, any more than robbers parceling out their shares of loot in advance should be treated as some sort of sanctified contract......................

Any melding of public debt into a private transaction must rest on the common but absurd notion that taxation is really "voluntary," and that whenever the government does anything, "we" are willingly doing it. This convenient myth was wittily and trenchantly disposed of by the great economist Joseph Schumpeter: "The theory which construes taxes on the analogy of club dues or of the purchases of, say, a doctor only proves how far removed this part of the social sciences is from scientific habits of mind." Morality and economic utility generally go hand in hand. Contrary to Alexander Hamilton, who spoke for a small but powerful clique of New York and Philadelphia public creditors, the national debt is not a "national blessing." The annual government deficit, plus the annual interest payment that keeps rising as the total debt accumulates, increasingly channels scarce and precious private savings into wasteful government boondoggles, which "crowd out" productive investments. Establishment economists, including Reaganomists, cleverly fudge the issue by arbitrarily labeling virtually all government spending as "investments," making it sound as if everything is fine and dandy because savings are being productively "invested." In reality, however, government spending only qualifies as "investment" in an Orwellian sense; government actually spends on behalf of the "consumer goods" and desires of bureaucrats, politicians, and their dependent client groups.................

I propose, then, a seemingly drastic but actually far less destructive way of paying off the public debt at a single blow: outright debt repudiation. Consider this question: why should the poor, battered citizens of Russia or Poland or the other ex-Communist countries be bound by the debts contracted by their former Communist masters? In the Communist situation, the injustice is clear: that citizens struggling for freedom and for a free-market economy should be taxed to pay for debts contracted by the monstrous former ruling class. But this injustice only differs by degree from "normal" public debt. For, conversely, why should the Communist government of the Soviet Union have been bound by debts contracted by the Czarist government they hated and overthrew? And why should we, struggling American citizens of today, be bound by debts created by a past ruling elite who contracted these debts at our expense? One of the cogent arguments against paying blacks "reparations" for past slavery is that we, the living, were not slaveholders. Similarly, we the living did not contract for either the past or the present debts incurred by the politicians and bureaucrats in Washington.

Although largely forgotten by historians and by the public, repudiation of public debt is a solid part of the American tradition. The first wave of repudiation of state debt came during the 1840s, after the panics of 1837 and 1839. Those panics were the consequence of a massive inflationary boom fueled by the Whig-run Second Bank of the United States. Riding the wave of inflationary credit, numerous state governments, largely those run by the Whigs, floated an enormous amount of debt, most of which went into wasteful public works (euphemistically called "internal improvements"), and into the creation of inflationary banks. Outstanding public debt by state governments rose from $26 million to $170 million during the decade of the 1830s. Most of these securities were financed by British and Dutch investors.......................................

the entire article is here

http://mises.org/daily/1423